Unlock Your People Potential with Faster Pay

Recruit talent and fill more shifts by providing fast access to earnings.

Whether you’re paying a barista at a coffee shop or a nurse at a hospital, accelerating pay to your employees has a direct effect on their engagement, productivity, and the level of service or care they can provide.

Choose the payout frequency

We support a range of pay frequencies and schedules, from payment right after each job or shift to daily or weekly payouts.

Shift-based: Pay out right after completed work.

Same-day: Automate daily payments for your team.

On-demand: Allow workers to withdraw up to 50% of their earned wages ahead of payday.

Weekly: Regular weekly or bi-weekly payments and direct deposits.

Off-cycle: Easily issue bonuses, rewards, or final paychecks—or correct payroll errors.

Simplify payday

No pre-funding or changes to payroll required. Make fast payments a breeze with one simple, streamlined platform.

Save money

Cut costs for you and your workers by saying goodbye to paper checks, costly paycards, and other fees for sending payments.

Go cashless

Eliminate cash handling and payment delays with digital payments, including cashless tips, mileage reimbursements, and other payments to employees.

Gain a competitive edge

Outpace your competitors by offering faster access to earnings.

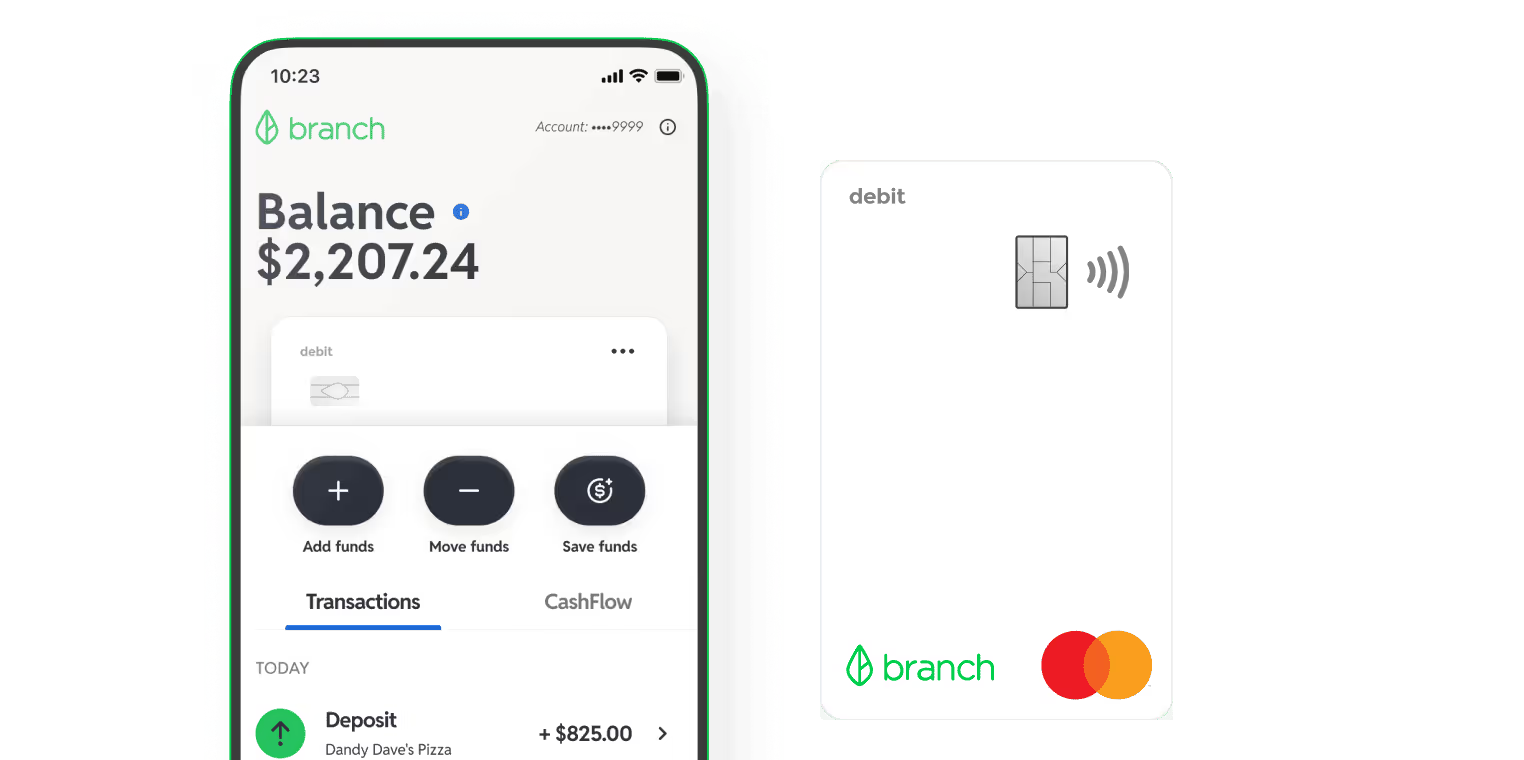

Good for Employers

Good for Employees

Unlock a Happier, More Productive Workforce